now loading...

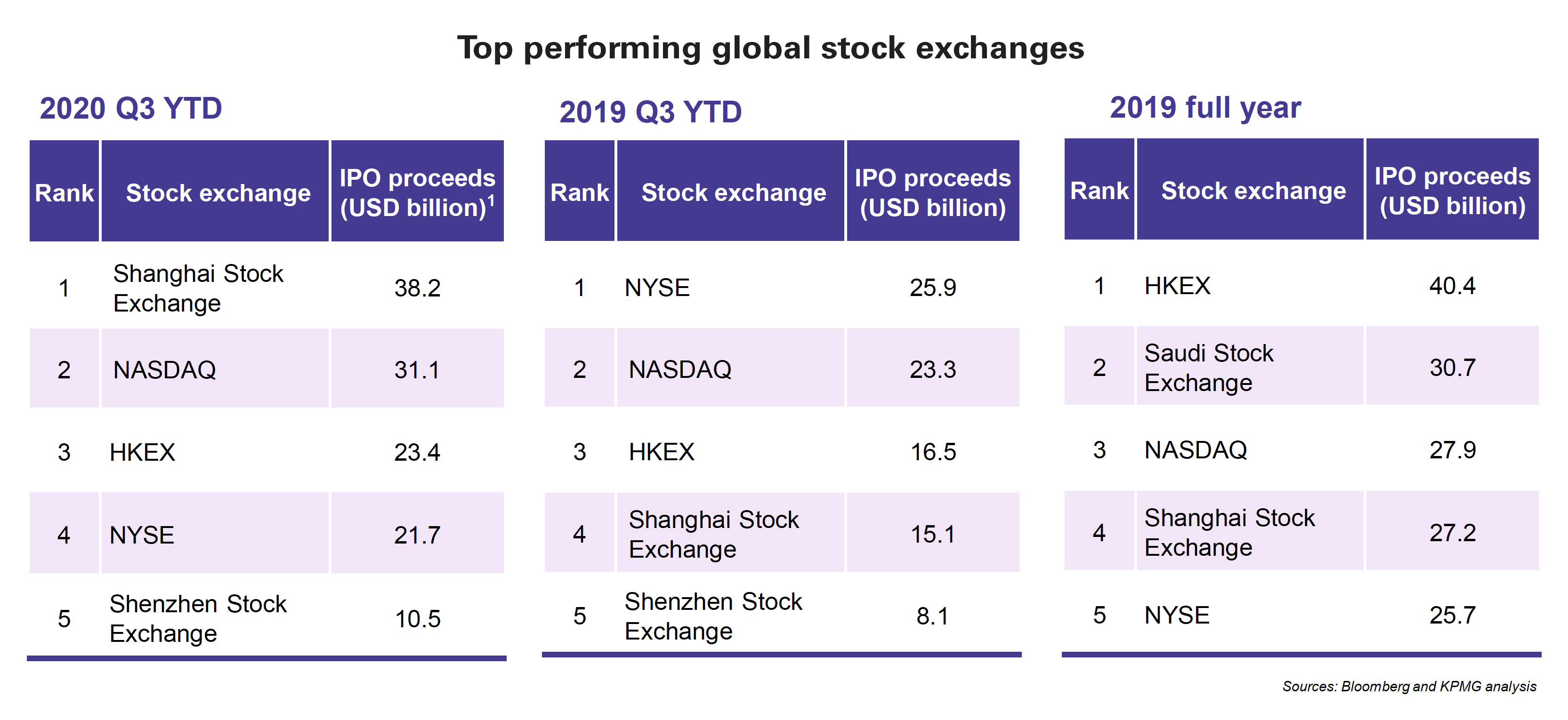

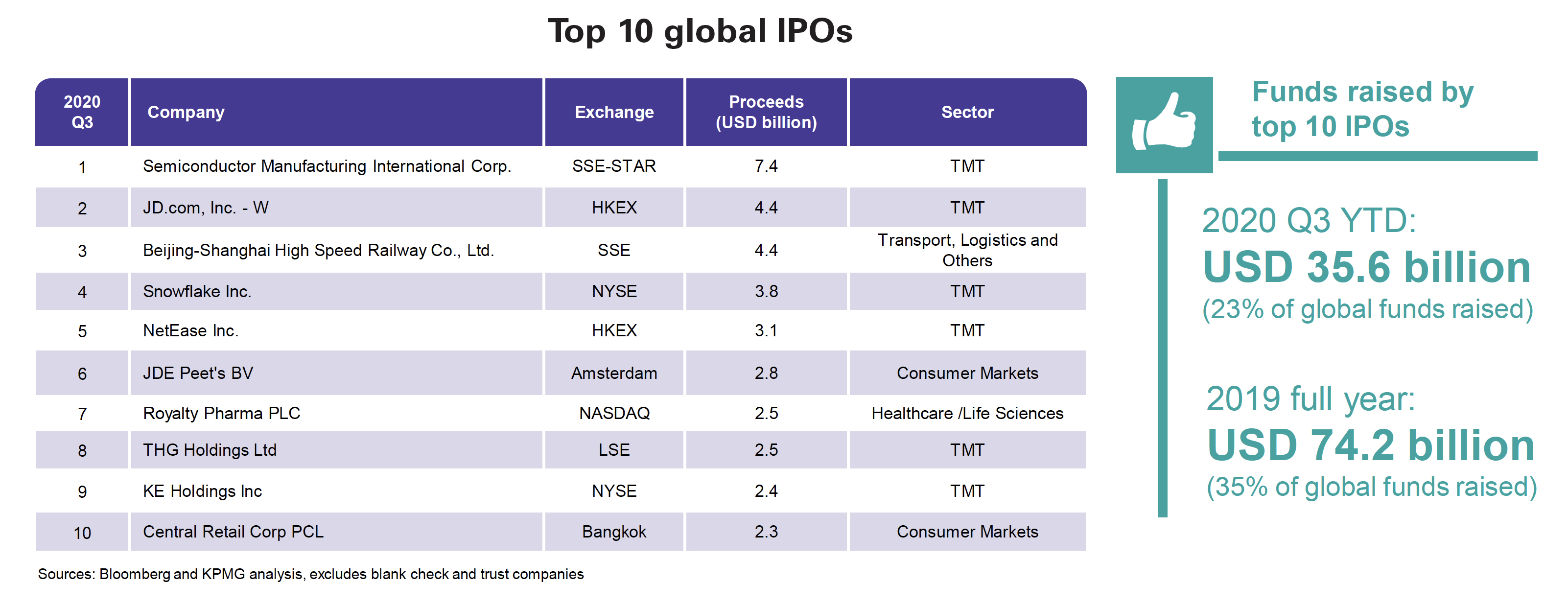

Mainland China and Hong Kong are expected to be the top destinations for initial public offerings this year after their strong showing in the first three quarters, KPMG says in its latest report on the IPO market. Shanghai and Hong Kong recorded the three largest IPOs in the third quarter, with Shanghai’s STAR Market hosting the listing of Semiconductor Manufacturing International Corp., which raised US$7.4 billion, followed by JD.com on the Hong Kong Stock Exchange ( US$4.4 billion ) and Beijing-Shanghai High Speed Railway Co., Ltd. in Shanghai ( US$4.4 billion ). The dual listing of Ant Group in Shanghai and Hong Kong is expected to give a further major boost to the two markets’ performance in terms of funds raised in the next quarter.

Globally, the IPO market has recorded a strong performance despite uncertainties resulting from the coronavirus pandemic and geopolitical tensions. Global IPO proceeds were expected to increase by over 30% by the end of the third quarter 2020, compared with the same period last year. The accounting firm attributes the huge growth mainly to a surge in fundraising in Asian markets, which offset a decline in proceeds in the European market.

The Shanghai Stock Exchange occupies the top spot globally in terms of both fundraising and number of listings year-to-date, followed by the Nasdaq and Hong Kong. Shanghai is boosted by the continuing popularity of the STAR Market, established in July 2019, which focuses on science and technology-themed equities.

The Shanghai and Shenzhen stock exchanges recorded 294 new listings for a combined 355.7 billion yuan ( US$52.12 billion ) in the first nine months of the year, up 154% from the same period last year. Building on the STAR Market’s success, reforms in the ChiNext, the Nasdaq-style subsidiary of the Shenzhen Stock Exchange, were completed during the period. The registration-based system places information disclosure at its core with a focus on serving innovative growth companies and startups. This further facilitates the growth of a multi-layered capital market, and enhances liquidity and investments in the A-share market, KPMG says.

In Shanghai, the STAR Market recorded 113 listings, raising 187.2 billion yuan, or 53 percent of funds raised in the A-share market for the first three quarters of the year. Since the first STAR market listing in July 2019 until now, 183 companies have listed on the board, raising a total of 269.6 billion yuan. Backed by a solid pipeline of over 200 listings, the STAR Market is expected to remain the major contributor to the A-share IPO market for the rest of 2020.

In Shenzhen, the first batch of registration-based IPOs of 18 enterprises debuted on August 24 this year. By the end of the third quarter, a total of 35 companies were expected to be listed under ChiNext’s new registration-based IPO system, raising a total of 34.5 billion yuan, or 43 percent of the funds raised in Shenzhen for the period.

The Hong Kong Stock Exchange, meanwhile, is benefiting from the increasing number of US-listed Chinese companies that are returning for secondary listings in the city. Seven such listings raised a combined US$13.1 billion, or 48% of funds raised in the bourse year-to-date.

During the nine-month period, Hong Kong saw the completion of 99 IPOs, raising a combined HK$210.6 billion ( US$27.17 billion ), up 57% from the same period last year. Seven companies have completed secondary listings in the city during the period, raising a total of HK$102.0 billion, or 48% of funds raised. These secondary listings single out Hong Kong as an even more important capital-raising venue with a growing ecosystem for innovation and new-economy companies, the accounting firm says.

With the groundwork laid since the listing reform in 2018, the ecosystem has been cultivating the development and fundraising for healthcare and life sciences companies, and Hong Kong has already become the second-largest biotech IPO market in the world and the largest in Asia. During the period, 13 healthcare/life sciences companies have been listed, raising a total of HK$42.2 billion, contributing 20 percent of total funds raised. Out of the 13 companies, seven pre-revenue biotech companies were listed under Chapter 18A, raising an aggregate of HK$19.1 billion.

Says Irene Chu, partner and head of new economy and life sciences, Hong Kong, at KPMG China: “IPOs in Hong Kong and mainland China will continue to be driven by new economy companies. As digital transformation has accelerated amid Covid-19, the demand for tech-enabled solutions in areas like telehealth, remote learning, drug development and logistics is growing. This is fueling the need for innovative companies to raise funds, especially in the TMT ( technology, media and telecoms ) and life sciences sectors.”

Moreover, Alibaba, Xiaomi and Wuxi Biologics have been added as constituents of the Hang Seng Index since September this year. Alibaba and Xiaomi are the first companies with weighted voting rights to join the blue-chip index. The move gives more weight to new economy companies on the traditionally finance-heavy index.