now loading...

The Asset Benchmark Research ( ABR ) is proud to announce the results of its inaugural Asian G3 Bond Syndicate Managers rankings.

We gathered the views of 180 of our most Astute Investors, who nominated up to five syndicate managers each and rated the criteria to be used in judging their performance.

Based on the survey criteria set by our most Astute Investors, Rishi Jalan from Citi ranks first, Elaine He from Morgan Stanley is second, and Carla Goudge from HSBC third. Cammy Lam from Bank of China International is the only syndicate manager from a Chinese bank to be ranked in the top 10. The ranking also shows that international banks still dominate the primary market.

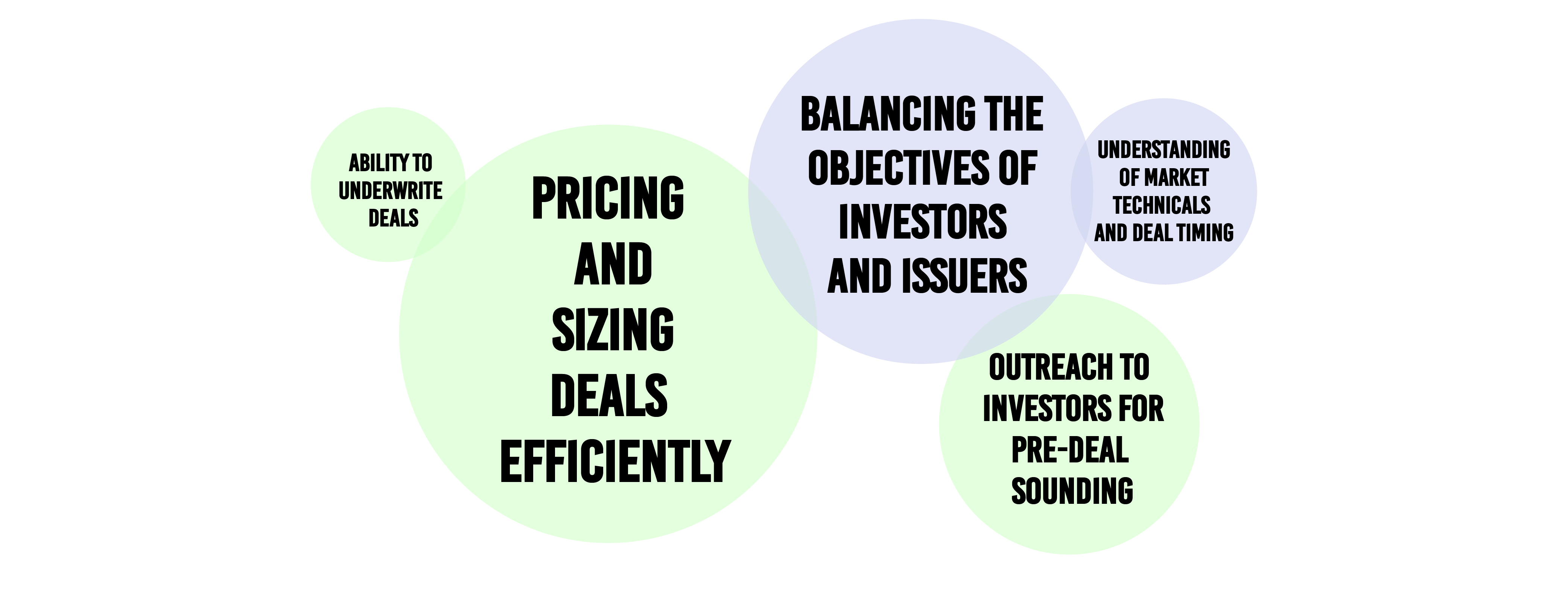

Among the criteria, “Pricing and sizing deals efficiently” tops the list. “Balancing the objectives of investors and issuers” comes in a close second. Syndicate managers’ outreach to investors for pre-deal sounding and their understanding of market technicals and deal timing also matter a lot to investors.

But the survey also reveals some criticisms of the primary bond market in the region, particularly the fairness of allocations. “There is a need to have a clear delineation between clients and syndicate banks,” comments an active G3 bond portfolio fund manager. “Currently, we have too many banks disguised as investors.”

In particular, investors call for transparency of access to the order book. “There should not be frequent over-inflated books,” says another investor. “When deals are over-subscribed, banks and their affiliates should not always be prioritized in terms of allocation.”

A buoyant market

The survey results are published in a year of unprecedented changes. Conducting a road show was part and parcel of an issuer’s fundraising exercise to meet investors and tell their credit story.

With the Covid-19 pandemic restricting travel and physical interaction, conference calls and video meetings have become the new normal in financial markets. This, however, has not impacted investors’ participation in new issues as indicated by the volumes so far this year.

According to data supplied by Refinitiv, Asian G3 bond issuance, outside Japan and Australasia, amounted to US$114.08 billion in the third quarter of 2020, representing an increase of 37.6% from US$82.93 billion in the same period a year ago. This was the highest third-quarter volume in Asian G3 bond issuance since 2010, as the market continued to brush aside the impact of Covid-19.

The higher volume of issuance was driven by investment grade credits, which took advantage of the continuing low interest rate environment and abundant market liquidity to print deals in larger amounts and in many instances with longer tenors. The flight-to-quality sentiment saw corporates pricing deals with maturities of 30 years, 40 years and even 50 years to raise long-term capital. Investors have been buying into these deals for yield pick-up, although there were issuers not joining the bandwagon as they refused to pay up.

It was a different story for the high-yield bond market whose volume of issuance fell by 41% to US$31 billion year-to-date, compared with US$53 billion in 2019, according to Moody’s Investors Service. Dominated by the Chinese property sector, issuances were relatively muted between February and April as many issuers had difficulties accessing the market and as investors stayed at the sidelines after having incurred mark-to-market losses.

Going forward, it remains to be seen how the introduction of the “Three Red Lines” designed to curb excessive borrowings by Chinese property companies will impact the issuance in the high-yield space.

Despite the cash-is-king sentiment prevailed in the early part of the year, most investors continued piling into the deals, enabling issuers, as the market re-opened, to tighten pricing. On the back of robust demand, several deals saw price compression by between 40bp and 60bp from initial price guidance to final pricing.

Thai Oil’s ten-year tranche of US$400 million was tightened by 60bps, from 2.45% area to 1.85%. The 30-year tranche of US$600 million was also tightened by 55 bps, from 4.30% area to 3.75%. Similarly, Tencent Music Entertainment Group’s five-year tranche of US$300 million and ten-year tranche of US$500 million were both tightened by 45 bps.

For a list of best syndicate managers, please click here