now loading...

In the ever-evolving landscape of venture capital ( VC ) and private equity ( PE ) funds, the need for innovative liquidity solutions has become more critical than ever. As a VC/PE fund nears the end of its term, managing the fund’s remaining illiquid assets often becomes a significant challenge. With the development of blockchain technology that enables the recording of ownership interests on a decentralized digital ledger ( tokenization ), we have seen an emerging market for tokenized fund offerings.

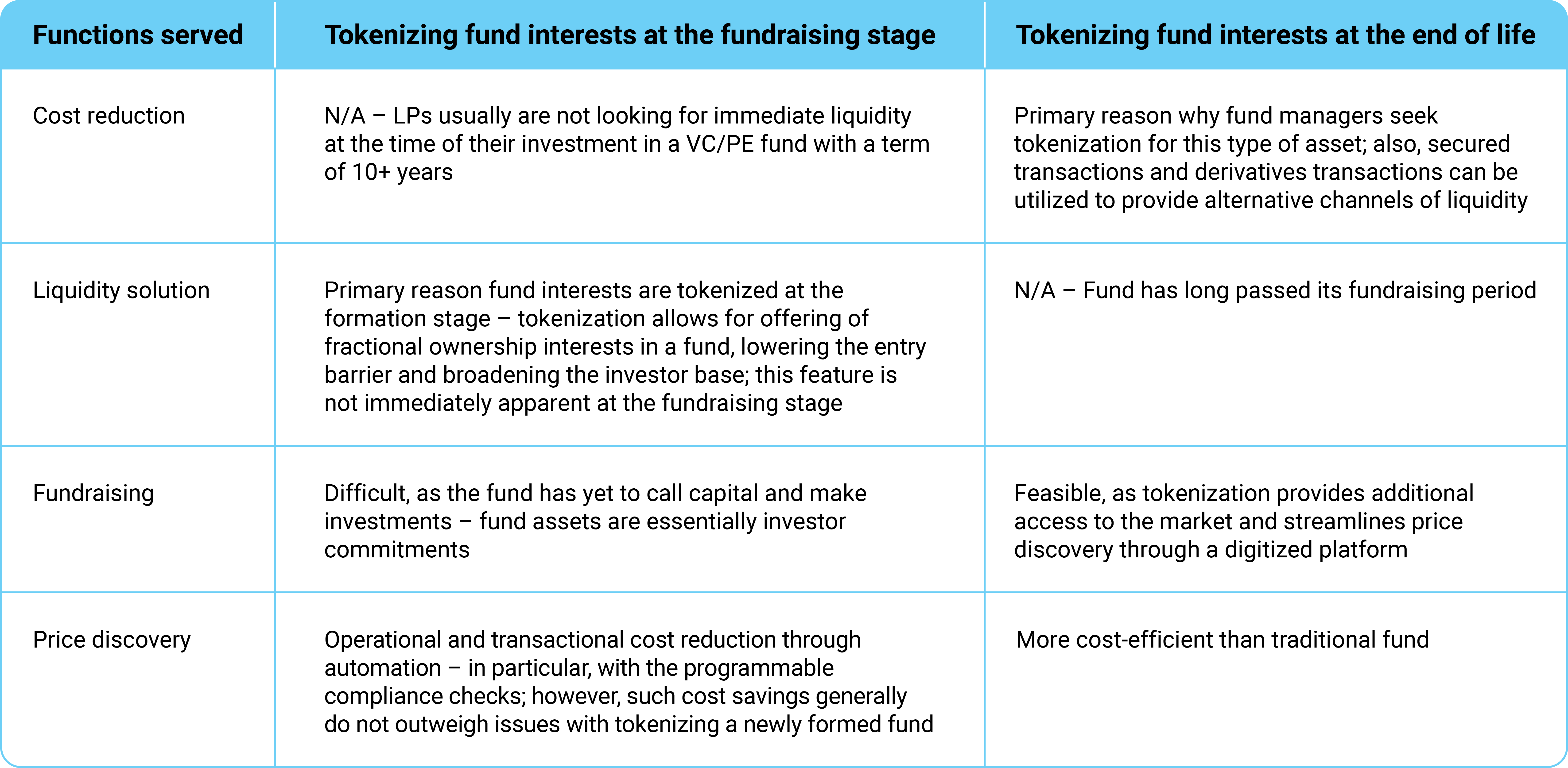

Tokenization provides more benefits for fully invested VC/PE funds near the end of their life cycle, versus at the fundraising stage, and approaching fund tokenization from such an angle could be the impetus for greater adoption of tokenization of this asset class.

Tokenization involves converting rights to real-world assets ( RWAs ) into a digital token on a blockchain. This process offers numerous benefits, including enhanced liquidity, transparency and efficiency in transactions. In the context of VC/PE funds, tokenization can revolutionize how fund interests are managed and traded by enabling instant transaction and settlement through smart contracts. However, we have not seen rapid adoption of blockchain and tokenization technology for newly organized VC/PE funds.

Challenges at the fundraising stage

Some of the reasons why we have not seen a great number of tokenized VC/PE funds are the same as in other asset classes – including, for example, network effects not being present at the moment, legal and regulatory uncertainties, and a lack of a central bank digital currency or an accepted trading venue, such as a licensed crypto exchange. More importantly, there has not been a compelling use case for tokenizing a VC/PE fund at the fundraising stage.

Benefits of tokenizing fully funded VC/PE funds

Compared to tokenizing a VC/PE fund at its inception when the fund itself is a blind pool, tokenization may be better suited for fully funded VC/PE funds and can serve as an alternative liquidity solution – in particular, for long-dated funds with illiquid assets that the GP has difficulty realizing.

Built-in tokenization flexibility in new fund formations

GPs forming new VC/PE funds may consider building future tokenization flexibility into the fund governance documents at the fund formation stage. The GP may prescribe a set of “master rules” for future tokenization of limited partnership interest after the fund is fully invested. Such “master rules” will allow the GP to control the key aspects of tokenization, such as jurisdiction, blockchain, exchange venue, liability, and investor and transaction white lists, while preserving flexibility for future implementations.

Tokenized fund vehicles offer a promising solution for fully funded VC/PE funds, particularly as they approach the end of their life cycle with illiquid assets. By taking advantage of the new tools to digitize assets, VC/PE funds can enhance liquidity, preserve value and provide flexibility for investors. This approach not only addresses the immediate challenges, but also might be the asset class that will set the stage to prime the market for more rapid adoption of tokenization of VC/PE funds in general.

Pang Lee, partner at law firm Cooley, advises on partnership, corporate and securities law matters related to the organization and investment in private funds and strategic investments in the tech industry. Shimeng Cheng, special counsel at Cooley, focuses on structured finance, asset-backed financing, synthetic derivatives and cryptocurrency investments. Joyce Wang, counsel at Cooley, covers all areas of corporate, partnership and securities law, with a focus on the representation of institutional investors in their global investments in private funds.