now loading...

China’s property market remains in a prolonged downturn despite government initiatives to revive the sector, with more developers turning to commercial real estate to staunch losses, a new report shows.

Primary home sales in 2025 are expected to drop by 8% from the previous year to 9 trillion yuan ( US$1.26 trillion ), followed by another 6% decline to 8.1 trillion yuan in 2026, according to projections by S&P Global.

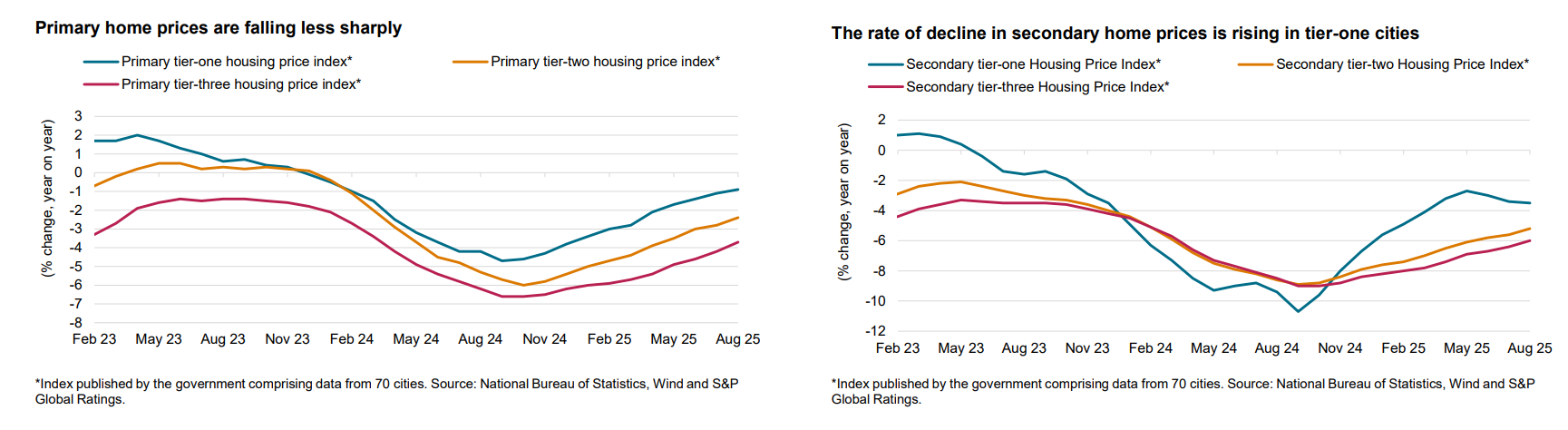

Compared to an expected 3% depreciation in primary housing prices this year, prices in the secondary market are likely to take a harder hit, a 7% slump.

“Even as nationwide investment in property development has been decreasing for a couple of years, the inventory level is still climbing, paired with declining rents that squeeze home prices,” says Edward Chan, director of corporate ratings at S&P Global, emphasizing that the market will only stabilize when the inventory stops increasing.

Despite the slow recovery, shallow upticks in primary housing prices have reversed the downward trend since November last year. However, home prices in Tier-1 cities fell again in Q2, compared to a steady uptrend in Tiers 2 and 3.

While the rising demand in the primary housing market is mainly driven by upgraders, secondary houses have lost much of their appeal due to lower competitiveness in usable space, design, and amenities.

“As upgraders sell their homes to purchase new ones, the supply of secondary homes will likely increase, and that could be the factor driving the decline in prices,” Chan says.

Land purchases surge

The backlog of unsold buildings, particularly in old developments, has increased the burden on private developers and tightened their liquidity. On the other hand, state-owned developers with adequate funding access have accelerated land acquisition to maintain their competitiveness.

“These newer projects can achieve higher sales rate than old inventories,” Oscar Chung, senior analyst, corporate ratings, at S&P Global explains.

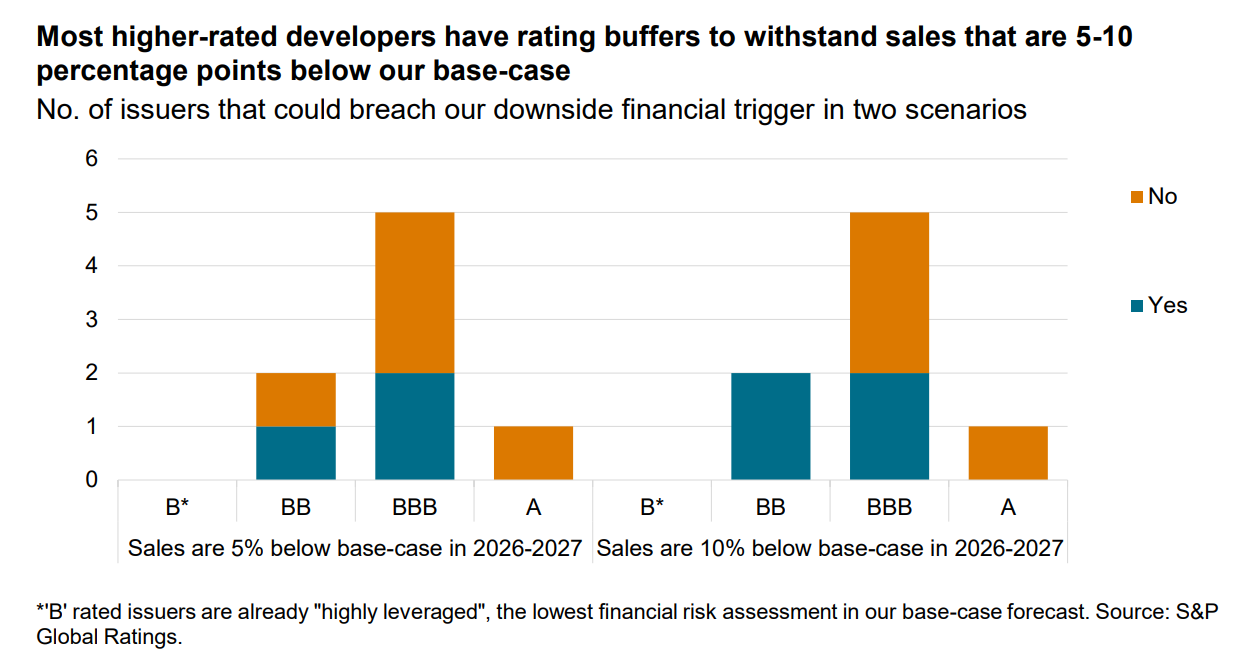

The robust demand for new land projects can boost and stabilize margins at the 20% level, but the breakneck pace of land purchases risks hurting credit profiles if sales fall short of expectation, Chung warns. Close to half of the state-owned developers have already purchased more than 80% of the full-year land acquisition estimate as of August.

Meanwhile, sales falling 10% below the base case will trigger the leverage alarm for triple B- and double B-rated developers, he notes, adding that this vulnerability is seen even among state-owned developers.

Reliance on retail properties

While the residential property sector struggles with sluggish sales, shopping malls provide stable rental income that counters the underperformance.

Rental opportunities are underpinned by organic growth and new mall openings, notes Wilson Ling, associate director, corporate ratings, at S&P Global, as he forecasts a 10% growth in retail rentals for 2026.

While a 5% expansion in retail sales is expected this year, it risks falling back to 4% in 2026, Ling warns, noting that consumer spending may lose momentum if the government ends its consumption-boosting initiatives, with the upcoming ones being less powerful than the stimulus launched in September last year.

Less resilient developers are likely to see rental incomes easing by more than half, which in turn will undermine their access to fresh funding and loan-to-value ratios.

“Recurring cash flow from rental would continue to be a steady force for some Chinese developers, but it’s not an easy task for retail landlords to protect the portfolio amid challenges in the retail market,” Ling notes.